BFG ruling destroys the self-employed model - prostitutes

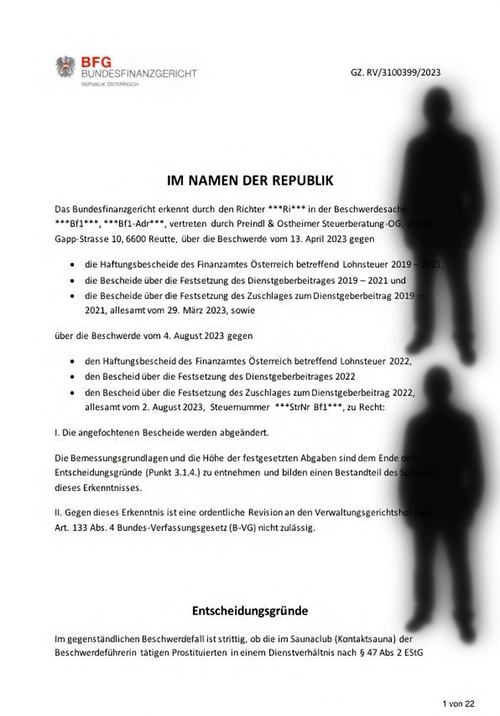

In its ruling of February 19, 2026 (GZ RV/3100399/2023), the Federal Fiscal Court (BFG) made a groundbreaking decision in lengthy appeal proceedings that has deeply concerned the red light industry in Austria - in particular operators of sauna clubs and contact saunas. The court essentially confirmed that the prostitutes working in the club were not self-employed, but in a non-self-employed employment relationship (Section 47 (2) EStG 1988). As a result, the operator is retroactively liable for wage tax, employer's contribution and supplement to the employer's contribution for the years 2019 to 2022. The contested decisions of the tax office were merely amended, not revoked. An ordinary appeal to the Administrative Court (VwGH) is expressly not permitted (Art. 133 para. 4 B-VG).

This ruling shocked many club operators because it shows how narrowly courts and tax authorities interpret the criteria for self-employment - and how quickly a supposedly "independent" model can topple. In the following, I analyze the decision in detail, explain the decisive features, the consequences for the industry and discuss possible adaptation strategies.

Course of proceedings and initial situation

The complainant (Bf) continued to run a sauna club (contact sauna) as a sole trader from September 2019, having previously been the managing director of a GmbH that ran the same business (later dissolved due to bankruptcy). The tax representative had already asked the tax office in 2017 whether the prostitutes were self-employed or not. The tax office replied back then (23.10.2017) that the activity was not self-employed.

Following payroll tax audits for 2019-2021 and 2022, the tax office issued liability notices (March/August 2023). The auditors found that the prostitutes were working independently, which is why the income was estimated and wage tax etc. was subsequently demanded. The complainant lodged an appeal and argued, among other things

- High fluctuation, switching between Austrian and German brothels

- No fixed working hours, free decision on attendance

- Own lingerie/sex toys for some

- No influence on prices

- SVS decisions (compulsory insurance pursuant to § 2 para. 1 no. 4 GSVG as an "employee in a trade of a special kind") are binding

- Double taxation possible for individual women

- Estimate (5 visits/day at € 150, 26 % tax rate) unrealistically high

The tax office dismissed the appeals in preliminary decisions (September 2023). The BFG essentially confirmed this (decision 2026).

The decisive criteria of the BFG: Why "non-self-employed"?

The court examined classic demarcation criteria between self-employed and non-self-employed activities (Section 47 EStG, VwGH/BFH case law). Decisive factors are instruction-bound and integration into the business organization of the operator.

The BFG considered the following indications of an employment relationship to be cumulative:

- Room allocation by the operator

With only 8 rooms, a free choice was illusory - de facto scheduling was mandatory. - Attendance list + notification to district administrative authority

Maintained by the club (partly a legal obligation), but an indication of control. - Cleaning of the rooms by club staff

No own responsibility of the prostitutes. - Minimum price requirement

The operator set minimum prices for sexual services. - Drinks commission (20%)

Incentive to encourage guests to consume in the club → Promotion of operating turnover. - Provision of equipment

Towels, condoms, sex toys etc. mainly from the club. - Partially specified working hours / attendance requirements

Combined with opening hours (15-01/03, rear entrance 10-03). - Advertising on homepage

Presentation of the "girls" (stage names, photos) by the club, reference to "not employees, but independent entrepreneurs" - but contradictory to reality.

The court weighed up counter-arguments (fluctuation, own resources in part, no fixed timetable), but did not consider them to be convincing.

Social security vs. tax law: No binding effect

Several prostitutes (including Ms. A, B, C, D) were subject to compulsory social security insurance (Section 2 (1) no. 4 GSVG). The BFG clarified: Such decisions do not automatically bind the tax office in wage tax proceedings. They are only binding in the case of specific audit procedures (e.g. joint income tax/SVV audit). This was not the case here.

The estimate of revenue

The tax office estimated:

- Attendance days (reported to BH) from 2019

- 5 room visits/day

- € 150 per visit (incl. VAT)

- 26 % income tax rate

The BFG considered this to be essentially justifiable (average values + surveys at BH). Only details were adjusted (exact figures in point 3.1.4 of the ruling). Criticism from the complainants (e.g. often only 30 min. at € 80, operation only from September 2019) was partially taken into account, but not decisive.

Consequences for the industry

This ruling is not a general ban on independent models in sauna clubs. It is an individual case, heavily dependent on the specific operating circumstances. Nevertheless, it sends a strong signal:

- Tax offices are increasingly examining payroll tax liability in comparable clubs.

- If instruction and integration features accumulate (as above), there is a risk of high additional payments (wage tax + employer contribution 4.5% + surcharge 0.45% + late payment surcharges + possible interest).

- VAT was estimated/fixed separately (other procedure RV/3100401/2023) - often on a net basis.

- Many clubs risk insolvency when back payments reach six figures.

The industry is faced with the choice of either strictly implementing self-employed models or openly recognizing employment relationships (with all obligations: Payroll tax deduction, social security contributions, vacation, protection against dismissal, etc.).

Possible adaptations - how to design "watertight" independently?

In order to strengthen independence, operators could implement the following (not conclusive, but in line with case law):

- No room allocation → free choice by prostitutes

- No minimum price requirements

- No beverage commission

- Prostitutes clean their own rooms

- No attendance lists/notifications by the club (only required by law, neutral)

- Own resources (lingerie, toys, condoms, etc.)

- No advertising with names/photos by the club (or clearly as an intermediary platform)

- Written contracts as rental or cooperation agreement (no employment contract)

- Free time management, no right to issue instructions

Whether this will hold in practice (especially with limited rooms and economic dependency) remains to be seen. Courts could continue to place economic reality above form contracts.

Conclusion and outlook

The BFG ruling RV/3100399/2023 marks a turning point. It shows that the "classic" sauna club model (room rental + control + commissions) can be qualified as dependent employment for tax purposes. Many operators fear chain reactions due to increased audits.

This could mean for the industry:

- Short-term high risk of subsequent payments and liquidity bottlenecks

- In the medium term, restructuring to pure room rental models or open employment relationships

- In the long term perhaps legal clarification (e.g. by adapting GSVG/EStG)

It remains to be seen whether similar cases will follow or whether the industry will adapt. The ruling can be viewed online and is sure to be the subject of intense debate.

Relevant sources / hyperlinks:

- BFG ruling RV/3100399/2023 - full text on FINDOK (BMF) - Original decision from 19.02.2026

- Austrian Income Tax Act 1988 - Section 47 (RIS) - Legal basis for the distinction between self-employed and non-self-employed persons

- GSVG § 2 para. 1 no. 4 - Compulsory insurance for prostitutes (RIS) - Regulation on compulsory social insurance in special types of business